In a quiet back office of a major insurance firm, an algorithm quietly flags a claim as potentially fraudulent—not because of human instinct, but because it recognized a subtle pattern across thousands of past cases. This is not science fiction. This is machine learning insurance, transforming risk assessment, fraud detection, and customer experience with scientific precision and data-driven insight.

Machine Learning Insurance: Redefining Risk Assessment

Traditional risk assessment in the insurance industry has long relied on actuarial tables, historical data, and demographic profiling. While effective in broad strokes, these methods often lack the granularity to capture individual risk profiles accurately. Machine Learning Insurance introduces a paradigm shift by enabling dynamic, real-time risk modeling based on vast datasets and complex behavioral patterns.

From Static Models to Dynamic Predictions

Legacy systems use static models that update infrequently and generalize risk across large populations. Machine learning, however, thrives on continuous learning. Algorithms such as Random Forest, Gradient Boosting, and Neural Networks analyze real-time inputs—driving behavior, health metrics, weather patterns, and even social media activity—to generate personalized risk scores.

- Dynamic risk models adapt to new data in real time

- Personalized premiums based on actual behavior, not averages

- Improved accuracy in predicting rare but high-cost events

For example, telematics in auto insurance now allows insurers to monitor braking patterns, speed, and mileage through IoT devices. Machine learning processes this data to assess driver safety far more accurately than age or location ever could.

Integration with IoT and Wearables

The synergy between machine learning and the Internet of Things (IoT) is revolutionizing health and life insurance. Wearable devices like Fitbit and Apple Watch collect continuous biometric data—heart rate, sleep quality, activity levels—which machine learning models interpret to assess health risks.

A 2023 study by NCBI demonstrated that machine learning models using wearable data could predict cardiovascular events with up to 89% accuracy, significantly outperforming traditional risk calculators.

“The future of underwriting isn’t just about what happened—it’s about what’s happening right now.” — Dr. Elena Torres, Data Scientist at InsurTech Labs

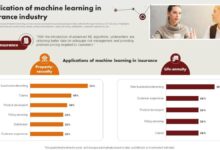

Machine Learning Insurance in Fraud Detection

Fraud costs the global insurance industry over $80 billion annually, according to the Coalition Against Insurance Fraud. Machine Learning Insurance is emerging as the most powerful weapon in combating this epidemic, detecting anomalies that human analysts might miss.

Pattern Recognition and Anomaly Detection

Machine learning algorithms excel at identifying subtle, non-linear patterns in data. In claims processing, models are trained on millions of historical claims—both legitimate and fraudulent—to recognize red flags such as inconsistent injury reports, suspicious timing, or unusual claimant behavior.

- Unsupervised learning detects unknown fraud patterns

- Supervised models classify claims with high precision

- Network analysis reveals organized fraud rings

For instance, clustering algorithms can group claims by geographic proximity, service provider, or legal representative, uncovering coordinated fraud schemes. A case study by Deloitte showed that machine learning reduced false positives in fraud detection by 40% while increasing detection rates by 25%.

Real-Time Claims Monitoring

Unlike rule-based systems that trigger alerts based on predefined thresholds, machine learning models operate in real time, continuously scoring claims as they are submitted. This allows insurers to intervene early, request additional documentation, or escalate for investigation before payment is made.

Advanced Natural Language Processing (NLP) models even analyze the text of claim descriptions, detecting linguistic cues associated with deception—such as overly detailed narratives or emotional inconsistency.

Personalized Customer Experience Through Machine Learning Insurance

Today’s consumers expect hyper-personalization. Machine Learning Insurance enables insurers to deliver tailored products, dynamic pricing, and proactive service, transforming the customer journey from transactional to relational.

Dynamic Pricing and Usage-Based Models

Gone are the days of one-size-fits-all premiums. Machine learning enables usage-based insurance (UBI), where pricing reflects actual behavior. In auto insurance, this means safer drivers pay less. In health insurance, it means rewards for maintaining fitness goals.

- Pay-as-you-drive (PAYD) and pay-how-you-drive (PHYD) models

- Incentivized wellness programs with real-time feedback

- Adaptive premiums that adjust monthly based on behavior

Progressive’s Snapshot program, powered by machine learning, has already enrolled over 20 million drivers, demonstrating the scalability of behavior-based pricing.

Chatbots and Virtual Assistants

Machine learning fuels AI-driven customer service tools that understand natural language, resolve queries instantly, and learn from every interaction. These virtual assistants handle everything from policy inquiries to claims initiation, reducing wait times and operational costs.

NLP models trained on vast corpora of insurance documents can extract key information from unstructured text, enabling chatbots to interpret complex policy language and provide accurate answers. A report by McKinsey found that AI-powered service tools can reduce customer service costs by up to 30% while improving satisfaction scores.

Machine Learning Insurance in Claims Processing Automation

Claims processing is one of the most labor-intensive and error-prone aspects of insurance. Machine Learning Insurance is automating this workflow, reducing processing time from days to minutes and minimizing human error.

Automated Damage Assessment

In property and auto insurance, image recognition models analyze photos of damage to estimate repair costs. Convolutional Neural Networks (CNNs) can identify dents, scratches, or structural damage with accuracy rivaling human adjusters.

For example, Lemonade, a digital insurer, uses AI to process claims in as little as three seconds. Their system analyzes submitted photos, cross-references policy details, and authorizes payments automatically—provided no red flags are detected.

- Image recognition for vehicle and property damage

- Automated estimation of repair costs

- Integration with repair networks for seamless service

Natural Language Processing for Claims Intake

When a customer files a claim via text or voice, NLP models extract critical information—date, location, parties involved, nature of loss—and populate structured fields in the claims system. This eliminates manual data entry and reduces processing delays.

Advanced models can even infer intent and urgency. For instance, a claim stating “I was rear-ended at a red light” is automatically tagged as high priority and routed to the appropriate department.

Machine Learning Insurance and Underwriting Transformation

Underwriting has traditionally been a slow, document-heavy process. Machine Learning Insurance accelerates this by automating data analysis, reducing reliance on manual reviews, and enabling near-instant policy issuance.

Automated Data Aggregation and Analysis

Modern underwriting platforms pull data from diverse sources—credit reports, medical records, public databases, and even satellite imagery. Machine learning models synthesize this information to generate risk scores in seconds.

For life insurance, AI can analyze electronic health records (EHRs) to assess mortality risk without requiring a medical exam. John Hancock, for example, offers “Vitality” policies that use AI to evaluate health data and offer premium discounts for healthy behaviors.

Reducing Bias and Improving Fairness

A major concern in AI adoption is algorithmic bias. However, when properly designed, machine learning models can actually reduce human bias in underwriting. By focusing on objective, measurable behaviors rather than proxies like zip code or name, ML systems promote fairness.

Techniques such as adversarial debiasing and fairness constraints are being integrated into underwriting models to ensure equitable treatment across demographics. A 2022 paper from arXiv demonstrated that fairness-aware ML models reduced racial disparities in auto insurance pricing by 60%.

Challenges and Ethical Considerations in Machine Learning Insurance

Despite its promise, Machine Learning Insurance faces significant challenges, including data privacy, model transparency, and regulatory compliance. These issues must be addressed to ensure sustainable and ethical deployment.

Data Privacy and Consent

Machine learning models require vast amounts of personal data, raising concerns about consent and data ownership. Insurers must comply with regulations like GDPR and CCPA, ensuring that data collection is transparent and purpose-limited.

- Explicit customer consent for data usage

- Data anonymization and encryption protocols

- Right to explanation and data deletion

Failure to address privacy concerns can erode trust and lead to regulatory penalties. A 2023 survey by PwC found that 68% of consumers would switch insurers if they felt their data was being misused.

Model Explainability and the ‘Black Box’ Problem

Many machine learning models, especially deep learning systems, operate as “black boxes,” making decisions that are difficult to interpret. In insurance, where decisions affect premiums and coverage, explainability is crucial.

Regulators like the NAIC (National Association of Insurance Commissioners) are pushing for “explainable AI” (XAI) frameworks. Techniques such as LIME (Local Interpretable Model-agnostic Explanations) and SHAP (SHapley Additive exPlanations) help insurers understand how models arrive at specific decisions.

“If you can’t explain the decision, you can’t defend it.” — Sarah Kim, Insurance Compliance Officer

Future Trends in Machine Learning Insurance

The evolution of Machine Learning Insurance is far from complete. Emerging technologies and shifting consumer expectations will drive the next wave of innovation, reshaping the industry in profound ways.

Integration with Blockchain for Trust and Transparency

Blockchain technology can enhance Machine Learning Insurance by providing immutable records of data transactions, model versions, and decision logs. This ensures auditability and builds trust in AI-driven decisions.

Smart contracts on blockchain platforms can automatically execute insurance payouts when machine learning models confirm claim validity, reducing fraud and administrative overhead.

Predictive Analytics for Proactive Risk Prevention

The future of insurance is not just about paying claims—it’s about preventing them. Machine learning models will increasingly be used to predict and mitigate risks before they materialize.

- Alerting homeowners to potential fire hazards based on sensor data

- Notifying drivers of high-risk weather conditions in real time

- Recommending health interventions before chronic conditions develop

This shift from reactive to proactive models aligns with the growing emphasis on wellness and safety in modern insurance.

What is Machine Learning Insurance?

Machine Learning Insurance refers to the application of machine learning algorithms in the insurance industry to improve risk assessment, fraud detection, claims processing, and customer personalization. It leverages data-driven models to automate decisions and enhance accuracy.

How does machine learning reduce insurance fraud?

Machine learning detects fraud by identifying anomalous patterns in claims data, using both supervised and unsupervised techniques. It can flag suspicious claims in real time, uncover organized fraud rings, and reduce false positives compared to traditional rule-based systems.

Is machine learning in insurance fair and unbiased?

While machine learning can introduce bias if trained on skewed data, it also offers tools to reduce human bias. With proper design, fairness constraints, and explainability techniques, ML models can promote more equitable insurance practices.

Can machine learning replace human underwriters?

Machine learning is automating many underwriting tasks, but human oversight remains essential for complex cases, ethical decisions, and regulatory compliance. The future lies in human-AI collaboration, not replacement.

What are the risks of using machine learning in insurance?

Risks include data privacy violations, algorithmic bias, lack of transparency, and over-reliance on automated systems. Insurers must implement robust governance, audit trails, and consumer protections to mitigate these risks.

Machine Learning Insurance is not a distant future—it is the present reality reshaping how risk is assessed, claims are processed, and customers are served. From detecting fraud with surgical precision to personalizing premiums based on real behavior, the integration of AI is making insurance smarter, faster, and fairer. Yet, with great power comes great responsibility. As algorithms gain influence, ensuring transparency, fairness, and consumer trust must remain paramount. The insurers who embrace machine learning not just as a tool, but as a transformative force guided by ethics, will lead the next era of the industry.

Further Reading: